Unsupervised learning 'credit card clients'

Understanding the behavior of clients of a product such as a credit card is vital to propose different marketing strategies or policies to management. Here we present, together with fourth-semester students of the Data Management subject, the unsupervised analytics application for a group of 9,000 credit card clients.

Image credit: freepik

Image credit: freepikToday credit cards are one of the most useful financial tools. Traditionally, having a credit card was a sign of having high economic power, but this has now changed. Now we have at our disposal a wide variety of types of credit cards. This is because not only banks can offer them, but some businesses have also started offering credit cards to adapt to the needs of consumers.

Credit cards have multiple functions and not everyone who has one implements it for the same purpose, so we want to know the behavior of use of approximately 9,000 active credit card holders, which have 17 variables of behavior, we carry out a segmentation of groups among the individuals to be studied, in relation to their behaviors; thus allowing us to simplify the complexity of the sample space with many dimensions while preserving its information.

In our database we take into account the following data…

Unsupervised analysis bases its training process on a data set that does not have a previously established label. Multivariate methodologies are relevant to finding answers about data.

The Principal Component Analysis (PCA) technique, applied by Karl Pearson, who was responsible for the application of statistics, as the PCA method in 1901; is used for quantitative variables, allowing to simplify the dimension of the data creating new variables to characterize each individual, these variables are called main components, which are given by the following linear combination

To see the classification of the model data set, Ward’s method is used, presented by Joe H. Ward, which considers all the clusters and the algorithm calculates the sum of the squared distances within each one, to later merge them and manage to minimize them.

Let’s go to R

We point out that the code and results are in spanish. This was made by Kleiner J. Balanta

Code

PACKAGES [Click to see the code]

library(tidyverse)

library(dendextend)

library(factoextra)

library(FactoClass)

library(corrplot)

library(caret)

library(stats)

library(dplyr)

DATA [Click to see the code]

Datos_Base<-read.csv("https://github.com/juniorjb5/Data/blob/main/TarjetasCredito.csv"

,header = TRUE, sep = "," ,dec = ".", row.names = 1) #En ese link consigues los datos

is.na(Datos_Base) # True: Nas y False: Datos

sum(is.na(Datos_Base)) #314 Na's

sum(complete.cases(is.na(Datos_Base))) #8950 Datos

# De 9264 observaciones, solo 8950 tienen observaciones sin Na's. Es decir, trabajamos

#con el 96,51% de las observaciones de la base de datos original. Aun es una buena base de datos.

Datos<-na.omit(Datos_Base)

View(Datos)

#Cambio de nombre de las columnas de la base de datos

Datos <- Datos %>%

rename(Saldo=BALANCE,Frec_Saldo=BALANCE_FREQUENCY,

Compras=PURCHASES,Compras_UnaVez=ONEOFF_PURCHASES,

Compras_aPlazos=INSTALLMENTS_PURCHASES,Efectivo_Adelantado=CASH_ADVANCE,

Frec_Compras=PURCHASES_FREQUENCY,Fre_Compras_UnaVez=ONEOFF_PURCHASES_FREQUENCY,

frec_Compras_aPlazos=PURCHASES_INSTALLMENTS_FREQUENCY,Frec_Efectivo_Adelantado=CASH_ADVANCE_FREQUENCY,

Num_trans_Efectivo_Adelantado=CASH_ADVANCE_TRX ,Num_trans_Compras=PURCHASES_TRX,

Limite_Credito=CREDIT_LIMIT ,Pagos_Realizados=PAYMENTS,Num_Min_Pagos_Realizados=MINIMUM_PAYMENTS

,Porcent_PagosCompletos_Realizados=PRC_FULL_PAYMENT

,Tenencia_Servicio=TENURE)

CORRELATION [Click to see the code]

matriz_correlacion<- cor(Datos)

print(matriz_correlacion)

Alta_Correlacion <- findCorrelation(matriz_correlacion,cutoff = 0,1)

print(names(Datos[,Alta_Correlacion]))

x11()

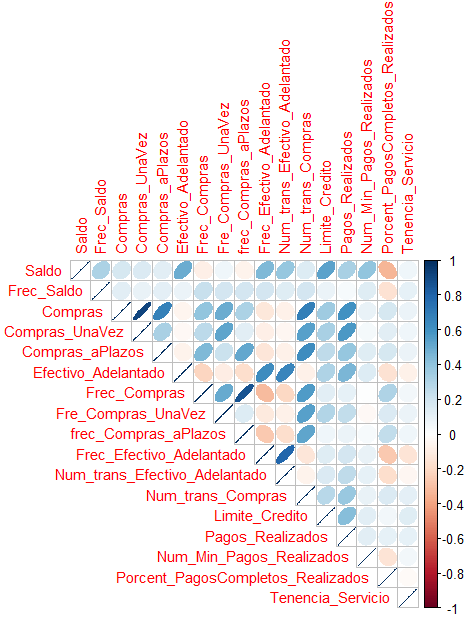

corrplot(cor(Datos), type="upper", method="ellipse", tl.cex=0.9)

The figure shows the correlation among all variables in the database

PCA [Click to see the code]

# Componentes: Varianza explicada

res.pca <- prcomp(Datos, scale = TRUE)

res.pca[[1]]

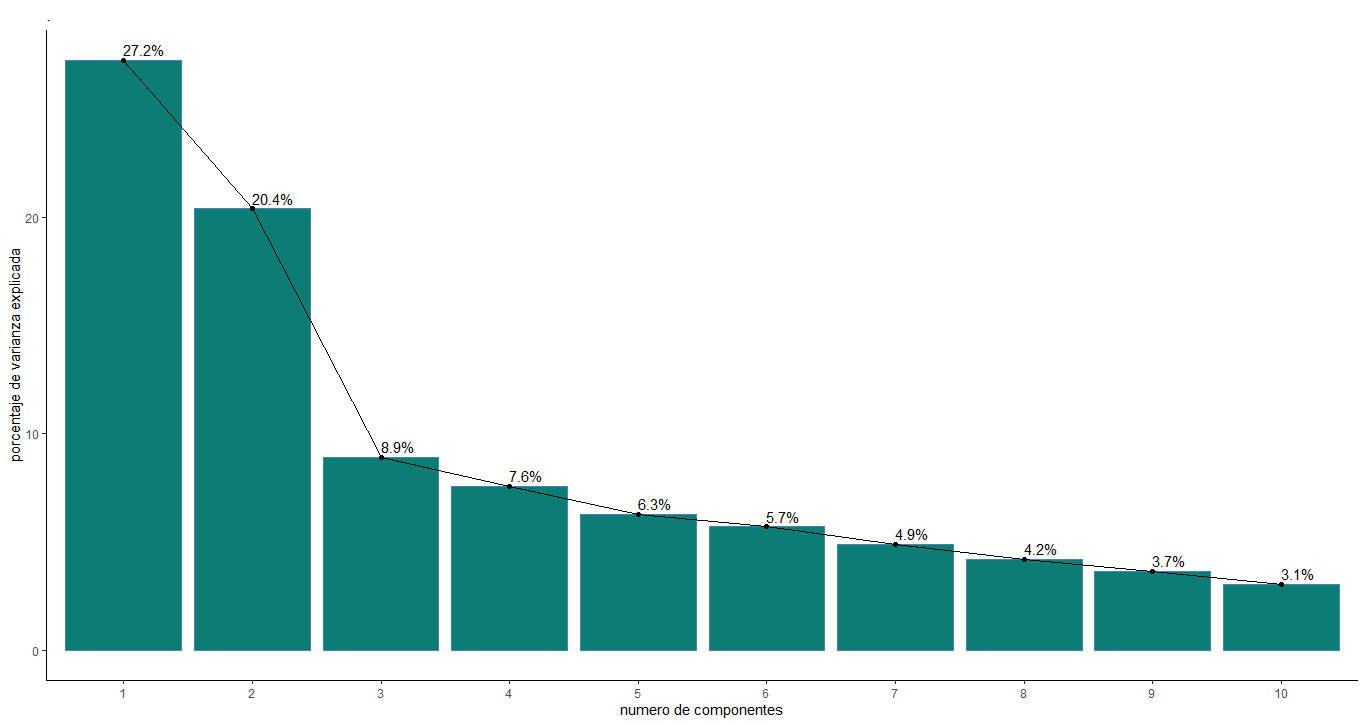

fviz_eig(res.pca,ylab = "porcentaje de varianza explicada",

xlab= "numero de componentes", main = "." ,barfill = "#0B7D75",addlabels = TRUE) + theme_classic()

There are different varieties of criteria that help to select the number of components, in this case it was decided to use one of the most famous called the Kaiser criterion. For this reason, the eigen values of the first 5 components were found, which are reflected in the following table

| PC 1 | PC 2 | PC 3 | PC 4 | PC 5 |

|---|---|---|---|---|

| 2.151580834 | 1.861083634 | 1.231306920 | 1.134686503 | 1.032969064 |

The Kaiser criterion recommends that 5 components should be selected. However, the value of the eigenvalues between components 3, 4 and 5 do not vary much compared to the first 2 components. Given this observation, it was decided to plot a bar chart with the percentage of variance or explanation provided by each component, in order to have a broader and more detailed view of the choice of components

The graph shows an interesting behavior, components 3, 4 and 5 do meet the Kaiser criterion as mentioned above, but between these the percentage of explained information does not have much difference, so it can be said that there is noise between them. . For this reason, it was decided to use 3 components, that is, we have a variance percentage of approximately 56.5% for our analysis.

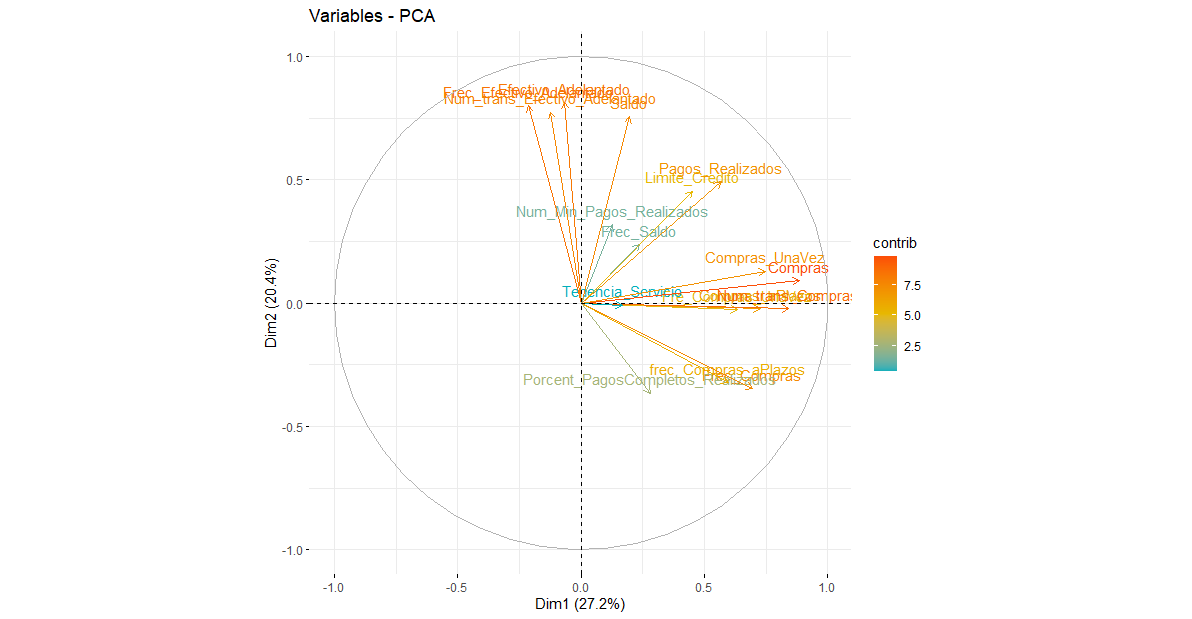

Based on the variables that most influence the explanation of the first component, this factor was named purchasing power; since its definition that groups and relates the variables. “Purchasing power, purchasing power or purchasing power is the amount of goods or services that can be obtained with a fixed amount of money depending on the price level”

Regarding the second component, it was called payment capacity, since in agreement with the Bank of Mexico (Banxico), there are users who have fixed monthly income and when making purchases they make their payments in cash or at the end of the month to avoid interest and build a good credit history, plus maintain access to the rewards and benefits on offer.

Finally, the third component was called excessive consumption, according to Marco Carrera, director of Market Studies of the National Commission for the Defense of Users of Financial Services (Condusef) in 2009, people who frequently buy from purchases that satisfy their basic needs are considered people who fall into the trend of consumerism, for which they see the need to pay the minimum cost of credit cards and thus maintain their credit limit and all the benefits that this entails.

PCA - GRAPHS [Click to see the code]

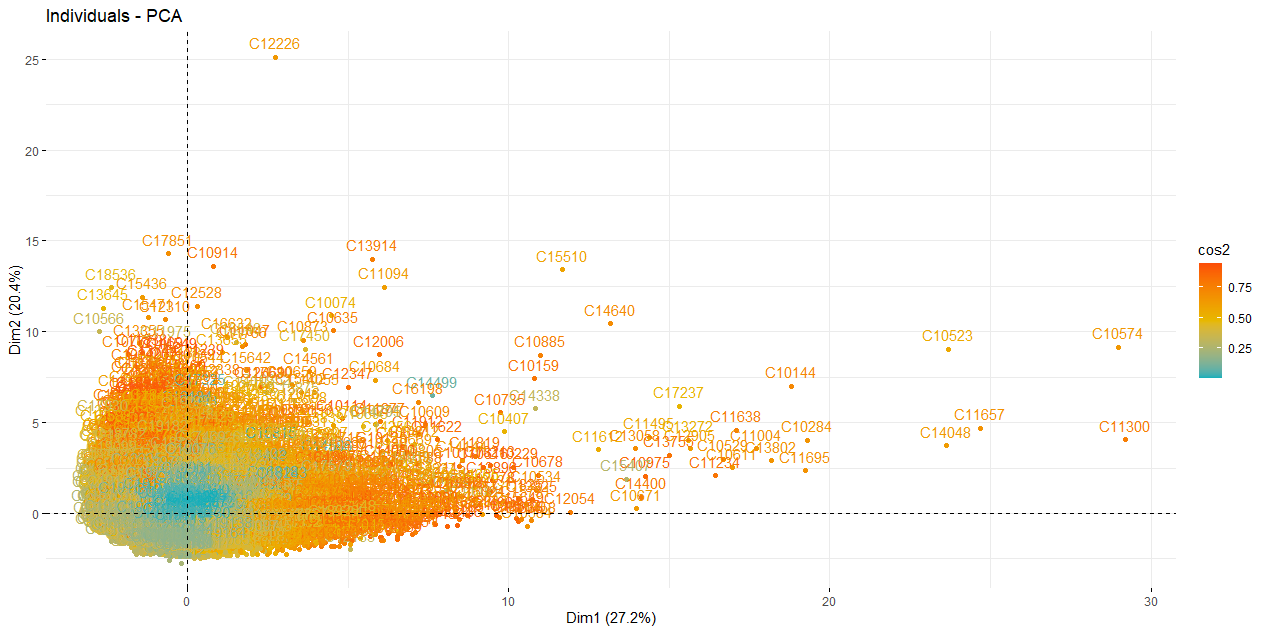

fviz_pca_ind(res.pca,

col.ind = "cos2", # Color by the quality of representation

gradient.cols = c("#00AFBB", "#E7B800", "#FC4E07"),

repel = FALSE # Avoid text overlapping

)

fviz_pca_var(res.pca,

col.var = "contrib", # Color by contributions to the PC

gradient.cols = c("#00AFBB", "#E7B800", "#FC4E07"),

repel = FALSE # Avoid text overlapping

)

fviz_pca_biplot(res.pca, repel = FALSE,

col.var = "#2E9FDF", # Variables color

col.ind = "#696969" # Individuals color

)

eig.val <- get_eigenvalue(res.pca)

eig.val #Valores propios de los componentes compuestos

res.var <- get_pca_var(res.pca)

res.var$coord # Coordinates

res.var$contrib # Contribuccion de las variables a los ejes

res.var$cos2 # Quality of representation

View(res.var$contrib[,1:3]) # Miro los 3 primeros factores

# Resultados por individuos

res.ind <- get_pca_ind(res.pca)

res.ind$coord # Coordinates

res.ind$contrib # Contribuccion a los componentes

res.ind$cos2 # Quality of representation

View(res.ind$contrib[,1:3]) # Miro los tres primeros factores

CLUSTERING [Click to see the code]

resultado_ACP<-FactoClass(Datos,dudi.pca)

3

3

4

resultado_ACP$cluster

NuevaBase<-data.frame(Cluster=resultado_ACP$cluster,Datos) # unir la nueva base de datos con la nueva variable cluster

View(NuevaBase)

plot(resultado_ACP$dudi) # Grafico del an?lisis

s.corcircle((resultado_ACP$dudi)$co)

s.label((resultado_ACP$dudi)$li,label=row.names(Datos)) #Graf. Individuos

s.label((resultado_ACP$dudi)$co,xax=1,yax=2,sub="Componente 1 y 2",possub="bottomright",) #Graf. Variables

s.label((resultado_ACP$dudi)$co,xax=1,yax=3,sub="Componente 1 y 3",possub="bottomright",) #Graf. Variables

s.label((resultado_ACP$dudi)$co,xax=2,yax=1,sub="Componente 2 y 1",possub="bottomright",) #Graf. Variables

s.label((resultado_ACP$dudi)$co,xax=2,yax=3,sub="Componente 2 y 3",possub="bottomright",) #Graf. Variables

s.label((resultado_ACP$dudi)$co,xax=3,yax=1,sub="Componente 3 y 1",possub="bottomright",) #Graf. Variables

s.label((resultado_ACP$dudi)$co,xax=3,yax=2,sub="Componente 3 y 2",possub="bottomright",) #Graf. Variables

x11()

scatter(resultado_ACP$dudi,xax=1,yax=2,sub="Componente 1 y 2",possub="bottomright") # Graf. Conjuntos

X11()

scatter(resultado_ACP$dudi,xax=1,yax=3,sub="Componente 1 y 3",possub="bottomright")

X11()

scatter(resultado_ACP$dudi,xax=2,yax=1,sub="Componente 2 y 1",possub="bottomright")

X11()

scatter(resultado_ACP$dudi,xax=2,yax=3,sub="Componente 2 y 3",possub="bottomright")

X11()

scatter(resultado_ACP$dudi,xax=3,yax=1,sub="Componente 3 y 1",possub="bottomright")

X11()

scatter(resultado_ACP$dudi,xax=3,yax=2,sub="Componente 3 y 2",possub="bottomright")

Grupo<-NuevaBase$Cluster

X11()

s.class((resultado_ACP$dudi)$li,Grupo,sub="Componentes 1 y 2",possub="bottomright",xax=1,yax=2,col=c(1,2,3,4))

X11()

s.class((resultado_ACP$dudi)$li,Grupo,sub="Componentes 1 y 3",possub="bottomright",xax=1,yax=3,col=c(1,2,3,4))

X11()

s.class((resultado_ACP$dudi)$li,Grupo,sub="Componentes 2 y 1",possub="bottomright",xax=2,yax=1,col=c(1,2,3,4))

X11()

s.class((resultado_ACP$dudi)$li,Grupo,sub="Componentes 2 y 3",possub="bottomright",xax=2,yax=3,col=c(1,2,3,4))

X11()

s.class((resultado_ACP$dudi)$li,Grupo,sub="Componentes 3 y 1",possub="bottomright",xax=3,yax=1,col=c(1,2,3,4))

X11()

s.class((resultado_ACP$dudi)$li,Grupo,sub="Componentes 3 y 2",possub="bottomright",xax=1,yax=2,col=c(1,2,3,4))

#importante

#DescripciÓn de los grupos (Análisis de medias)

resultado_ACP$carac.cont

Dendogram

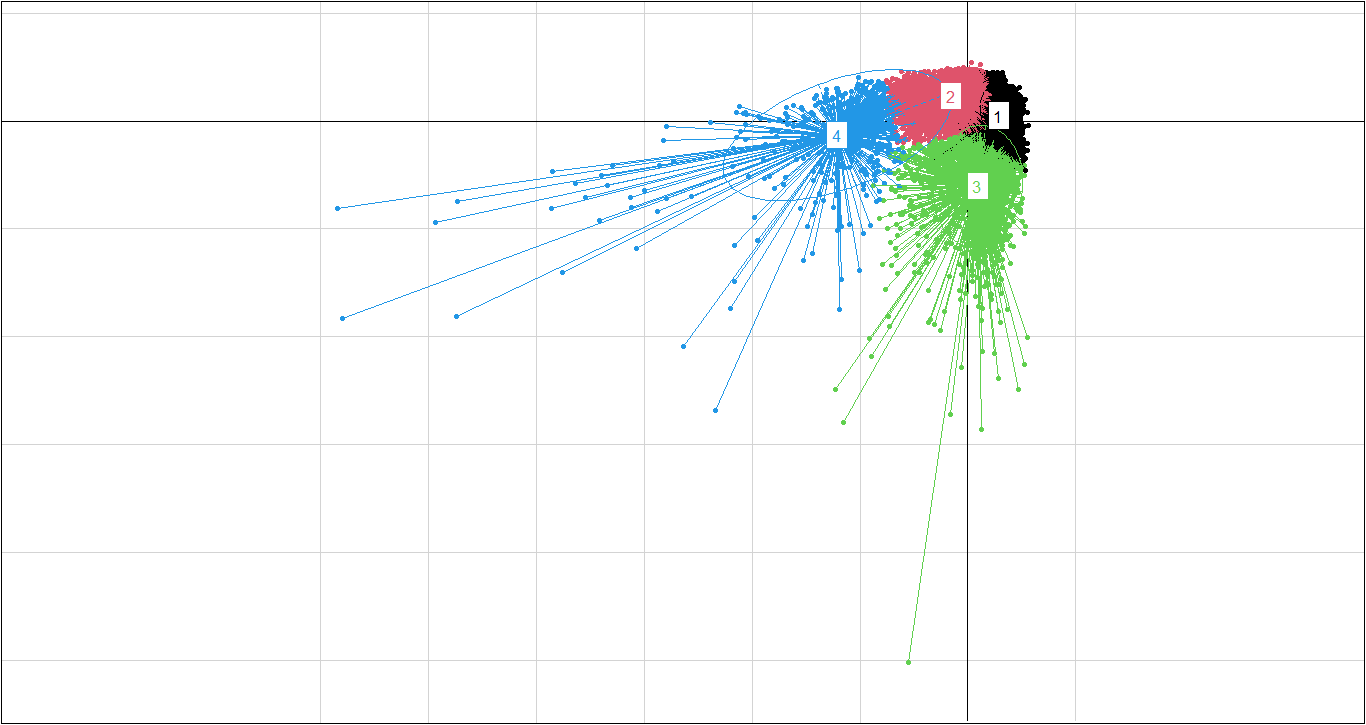

PC1 vs PC2

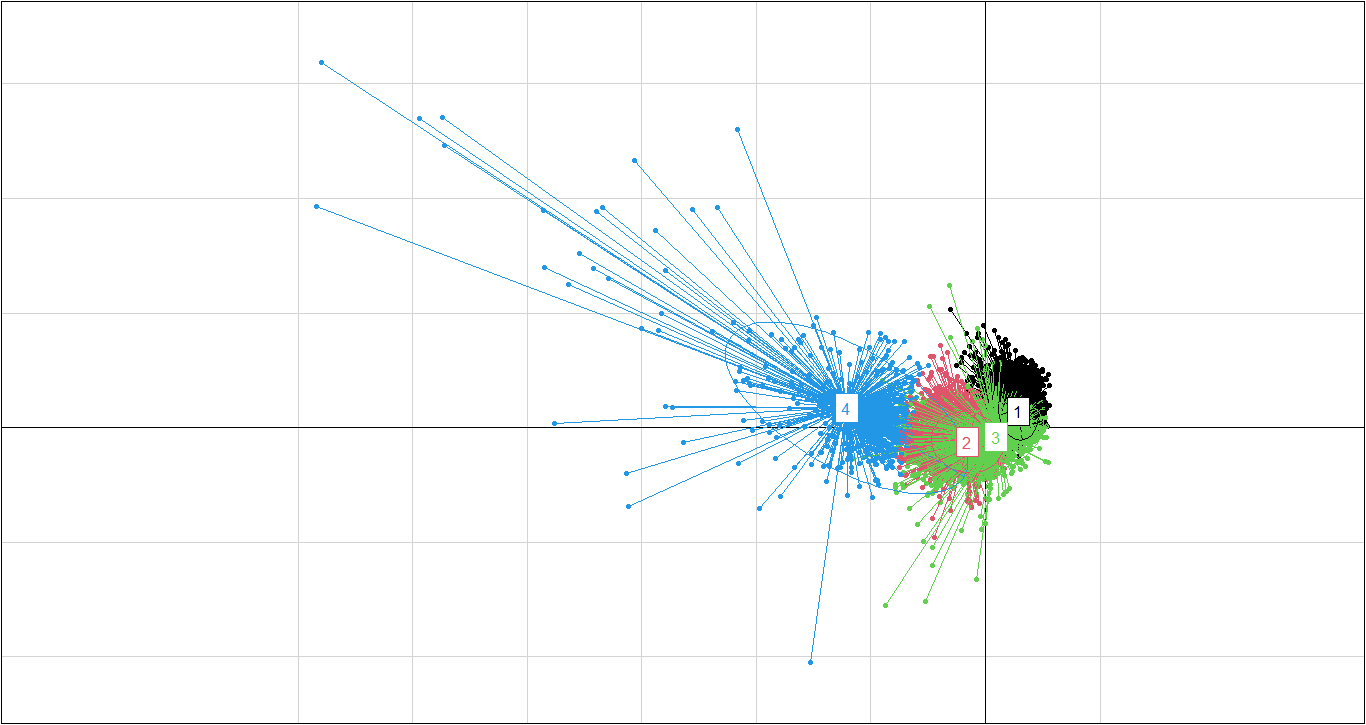

PC1 vs PC3

Class characterization

class: 1

Test.Value Class.Mean Frequency Global.Mean

Frec_Compras 68.218 0.938 2657 0.496

frec_Compras_aPlazos 61.895 0.767 2657 0.369

Fre_Compras_UnaVez 40.837 0.404 2657 0.206

Compras_aPlazos 34.321 929.010 2657 420.844

Compras 28.956 2038.379 2657 1025.434

Porcent_PagosCompletos_Realizados 25.250 0.280 2657 0.159

Frec_Saldo 24.426 0.977 2657 0.895

Compras_UnaVez 18.570 1109.784 2657 604.901

Limite_Credito 13.143 5298.450 2657 4522.091

Pagos_Realizados 5.278 2032.412 2657 1784.478

Saldo -7.423 1350.131 2657 1601.225

Efectivo_Adelantado -21.528 256.949 2657 994.176

Frec_Efectivo_Adelantado -28.902 0.043 2657 0.138

------------------------------------------------------------

class: 2

Test.Value Class.Mean Frequency Global.Mean

Frec_Efectivo_Adelantado -10.482 0.118 4960 0.138

Num_Min_Pagos_Realizados -14.953 535.657 4960 864.305

Porcent_PagosCompletos_Realizados -16.299 0.115 4960 0.159

Efectivo_Adelantado -18.377 633.015 4960 994.176

Compras_UnaVez -25.412 208.401 4960 604.901

Pagos_Realizados -28.894 1005.618 4960 1784.478

Saldo -29.143 1035.473 4960 1601.225

Frec_Saldo -31.424 0.835 4960 0.895

Compras -35.002 322.735 4960 1025.434

Compras_aPlazos -36.037 114.633 4960 420.844

Limite_Credito -36.397 3288.275 4960 4522.091

Fre_Compras_UnaVez -37.545 0.102 4960 0.206

frec_Compras_aPlazos -50.555 0.182 4960 0.369

Frec_Compras -55.501 0.290 4960 0.496

------------------------------------------------------------

class: 3

Test.Value Class.Mean Frequency Global.Mean

Efectivo_Adelantado 60.918 4968.608 942 994.176

Frec_Efectivo_Adelantado 60.158 0.511 942 0.138

Saldo 53.513 5049.907 942 1601.225

Limite_Credito 32.142 8139.124 942 4522.091

Pagos_Realizados 24.556 3981.927 942 1784.478

Num_Min_Pagos_Realizados 22.039 2472.399 942 864.305

Frec_Saldo 12.669 0.976 942 0.895

Compras_UnaVez -4.497 371.965 942 604.901

Fre_Compras_UnaVez -6.205 0.149 942 0.206

Compras -6.405 598.583 942 1025.434

Compras_aPlazos -6.882 226.726 942 420.844

Porcent_PagosCompletos_Realizados -13.818 0.033 942 0.159

frec_Compras_aPlazos -14.172 0.195 942 0.369

Frec_Compras -15.868 0.300 942 0.496

------------------------------------------------------------

class: 4

Test.Value Class.Mean Frequency Global.Mean

Compras 63.180 16559.006 77 1025.434

Compras_UnaVez 57.402 11573.696 77 604.901

Pagos_Realizados 44.627 16516.810 77 1784.478

Compras_aPlazos 43.863 4985.310 77 420.844

Limite_Credito 20.325 12959.740 77 4522.091

Fre_Compras_UnaVez 17.557 0.804 77 0.206

Saldo 12.270 4518.465 77 1601.225

Frec_Compras 9.616 0.934 77 0.496

frec_Compras_aPlazos 9.027 0.777 77 0.369

Porcent_PagosCompletos_Realizados 7.584 0.414 77 0.159

Num_Min_Pagos_Realizados 5.865 2442.863 77 864.305

Frec_Saldo 3.347 0.974 77 0.895

Frec_Efectivo_Adelantado -2.465 0.081 77 0.138

The first class is made up of clients with the highest credit card balance, it can be inferred that they have a good salary or earn a lot of money. These people prefer not to pay for their purchases with a credit card, they prefer to withdraw cash in advance to make said purchases. Your credit limit is very high, since your income is high and the time with which you pay your cash advances is very low. In short, they are rich people who do not buy with their card, perhaps so that there is no record of their purchases. In terms of social level, they are high-income people who prefer to avoid registering their bank transactions. This class of clients was classified as passive clients.

The second class is made up of very low balance clients, actually the second lowest among the classes. They are the class with the lowest rate of purchases, whether in instant purchases or installment purchases. The aforementioned is reflected in your credit limit, since you earn little money, do not enter installments and have a low rate of payments through your cards, your credit limit is relatively low. Socially, they are low-income people who do not have the possibility of accessing constant purchases, they prefer to save their money and not take risks. These clients were called inactive clients.

The third class is made up of clients with the lowest balance on the card but who make cash purchases, that is, they do not earn much money and their salary on the card is low, however, they continue to consume, make purchases frequently, whether for goods or services, by means of a credit card, generally in installments or installments because it is not possible for them to pay instantly due to the little money they have in their accounts. In addition, the payment limit is lower than the global average for all clients, due to their low income level. It is not the lowest credit limit among the classes because, by frequently making installment purchases, their credit history is good, however, the time in which they pay their debts is not favorable for their credit limit. They are low-income people who are passionate about indulging their frequent desires, even if that means paying installments. They were called active clients.

In the fourth class are present clients who use credit cards more, since they maintain a high rate of frequent purchases instantly or in installments, because they handle a large amount of money and keep a balance to later acquire any good or service. , which is why they have a high profile in the banking institution and benefit from obtaining a higher credit limit, in addition to withdrawing very little cash in advance. Socially, they were called high-income people who spend their money to satisfy their tastes, apart from their basic needs. These people are potential clients.

Market strategies

Passive clients, they have very low purchases, due to the lack of information on promotions and discounts, for which, from the user’s database, a telephone number can be contacted and begin to make informative use of that means of communication. Likewise, the advisors can be in contact by means of telephone calls, in order to spread the information and make sure that the user obtains the benefits. To motivate you, you can initially generate promotions, accumulation of points that can later be redeemed in some good or cash refunds.

Inactive clients, an incentive plan can be implemented, where an order of quotas is proposed, which allow them to go to certain places to access a product as a reward for the high use of credit cards, this strategy can be carried out carried out in the people who buy the most and with that constant use is promoted.

Active clients, by maintaining constant purchases, the accumulation of points can be implemented, either to obtain a free product or with good discounts and the exclusivity of participating in raffles of some good, such as appliances. Likewise, up to 3 installments without interest can be managed, with the aim that the client is motivated and makes their purchases.

To encourage the best credit card clients, rewards or incentives can be generated for the number of purchases made, whether monthly or semi-annually, likewise, miles can be accumulated so that users can obtain tickets without high costs on planes and in the VIP area, as well as tickets to concerts, entertainment areas, restaurants, among others.

New clients

PREDICT [Click to see the code]

ind.test <- Datos[8632:8636, 1:17] #5 clientes para realizar la prediccion

head(ind.test)

ind.test.coord <- predict(res.pca, newdata = ind.test)

ind.test.coord[, 1:3] # Miro los primeros dos componentes

# Utilizo el gráfico anterior y le anexo los nuevos individuos

p <- fviz_pca_ind(res.pca, repel = TRUE)

fviz_add(p, ind.test.coord, color ="blue")

nuevospuntos<-data.frame(ind.test.coord)

NP2<-data.frame(names = rownames(nuevospuntos), nuevospuntos)

Newgrafico<-data.frame((resultado_ACP$dudi)$li , Grupo)

X11()

#PC1 ; PC2

ggplot(Newgrafico, aes(x = Axis1, y = Axis2, color = Grupo)) +

geom_point() +

geom_point(NP2, mapping=aes(x=PC1,y=PC2, color = "Nuevos",

label = names), size=5.5)+ theme_bw()

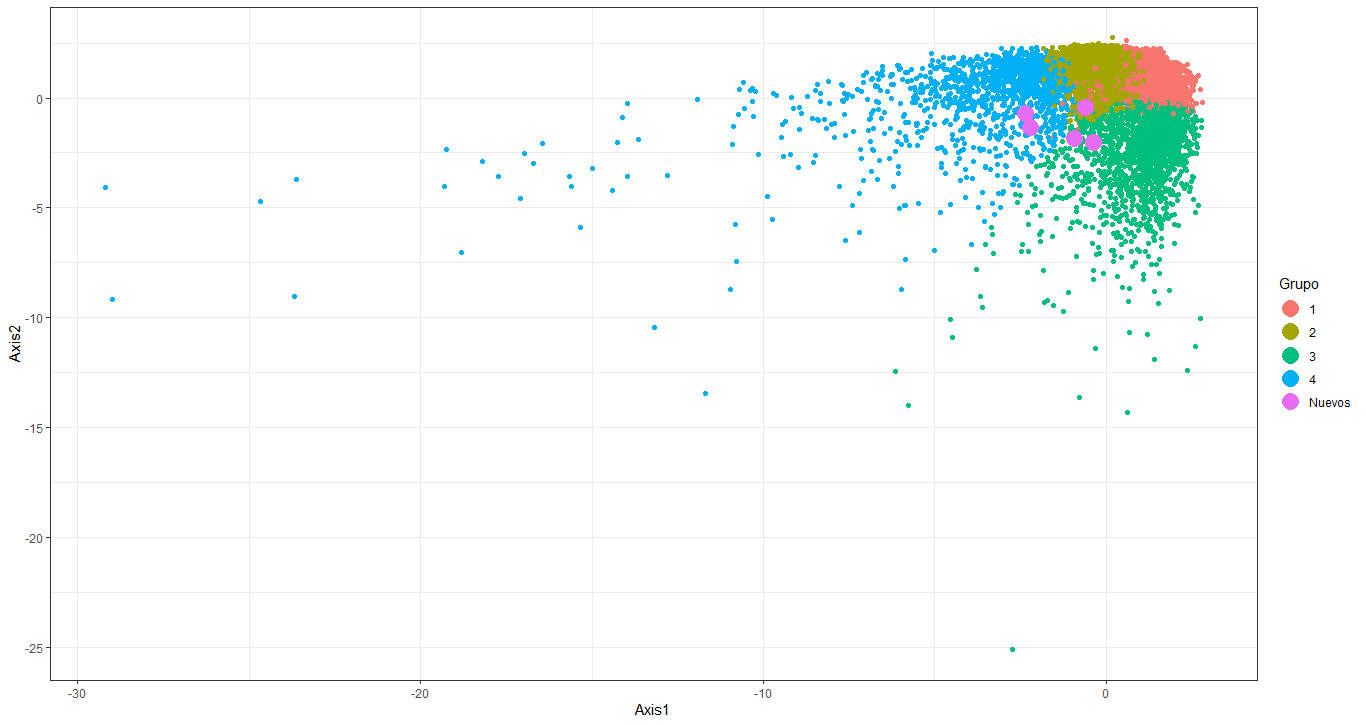

We managed to classify customers into classes depending on their characteristics in the use of the credit card. However, the banking institution will not always have the same number of clients and these will not always present the same behavior, therefore, it is necessary that the created model has the ability to predict to which group a client with new characteristics should belong management regarding the use of your credit card.

That said, a classification test was carried out with 5 clients without a group, to evaluate the effectiveness of the model at the time of cataloging. This test is done graphically, incorporating new clients represented by purple dots in the plans previously designed in graph 4; It is worth mentioning that the value of the characteristic variables of the five clients with respect to the use of their credit card is known.

The visualization of the new clients in the groups is better illustrated in the plane composed of components 1 and 2, for this reason the main analysis was carried out with this plane. Now, among these 5 clients, the model classified 3 of them as members of group 2 (inactive clients), and the rest as members of group 3 (active clients).

Supervised learning

We realize a supervised analyses using the classification founded in the clustering. We use 75% of the data as training, and 25% as test.

The class that better is classified is 4. Potencial Clients.

KNN [Click to see the code]

NuevaBase <- NuevaBase %>%

rename(grupo = Cluster ) %>%

mutate_at(c("grupo"), ~as.factor(.))

IndexEntrena<-createDataPartition(y = NuevaBase$grupo, p=0.75 , list = FALSE)

SP_entrena <- NuevaBase[IndexEntrena,]

SP_test <- NuevaBase[-IndexEntrena,]

SP_knnEntrenado <- train(grupo ~ .,

data = SP_entrena,

method = "knn",

tuneLength = 20)

class(SP_knnEntrenado)

SP_knnEntrenado

X11()

plot(SP_knnEntrenado)

SP_ctrl <- trainControl(method="cv", number = 5) #Metodo de validación cruzada

SP_knnEntrenado <- train(grupo ~ .,

data = SP_entrena,

method = "knn",

tuneLength = 20,

trControl = SP_ctrl,

preProcess = c("center", "scale"))

SP_knnEntrenado

x11()

plot(SP_knnEntrenado) # Aprece un nuevo k optimo! K=7

plot(SP_knnEntrenado,pch=8 ,bty="1",bg="seagreen2

nos", ylab = "Precision (Validación Cruzada)", xlab= "vecinos" ) #Grafica de K vs Precision

SP_knnPrediccion <- predict(SP_knnEntrenado, newdata = SP_test)

SP_knnPrediccion %>%

head(50)

prob_knnPrediccion <- predict(SP_knnEntrenado, newdata = SP_test, type= "prob")

prob_knnPrediccion %>%

head(10) #Probabilidades para catalogar a que grupo pertenece el cliente

confusionMatrix(SP_knnPrediccion, SP_test$grupo)

Confusion Matrix and Statistics

Reference

Prediction 1 2 3 4

1 463 118 4 1

2 182 1099 51 0

3 19 23 180 0

4 0 0 0 18

Overall Statistics

Accuracy : 0.8156

95% CI : (0.7986, 0.8317)

No Information Rate : 0.5746

P-Value [Acc > NIR] : < 2.2e-16

Kappa : 0.665

Statistics by Class:

Class: 1 Class: 2 Class: 3 Class: 4

Sensitivity 0.6973 0.8863 0.76596 0.947368

Specificity 0.9177 0.7462 0.97816 1.000000

Pos Pred Value 0.7901 0.8251 0.81081 1.000000

Neg Pred Value 0.8721 0.8293 0.97159 0.999533

Prevalence 0.3077 0.5746 0.10890 0.008804

Detection Rate 0.2146 0.5093 0.08341 0.008341

Detection Prevalence 0.2715 0.6172 0.10287 0.008341

Balanced Accuracy 0.8075 0.8162 0.87206 0.973684

Made by 🙌

📚 Kleiner J. Balanta - Student of Industrial Engineering

(Universidad del Valle)

📚 Laura V. Cicery - Student of Industrial Engineering

(Universidad del Valle)

📚 Sofia Vivas - Student of Industrial Engineering

(Universidad del Valle)

📚 Carlos A. Cruz - Student of Industrial Engineering

(Universidad del Valle)

Orlando Joaqui Barandica

PhD Industrial Engineering

My research interests include energy markets, business analytics, quantitative finance, applied econometrics and statistical, and data visualization.